BLOG. 2 min read

With a growing portion of the world’s financial assets allocated to passive investment strategies, exchange-traded funds (ETFs) have become a critical part of the modern finance landscape. For example, some institutional investors now often use ETFs to steer their core international allocations with great flexibility. Other institutions invest in these liquid financial vehicles as cost-efficient trackers of their domestic market indices. ETFs represent important sources of daily market liquidity as well.

While the “passive investment” label can still fit most ETF products, a lot of their manufacturers would better describe these as “actively managed” index funds. As early adopters of advanced computing techniques, ETF managers have long used optimization as a part of their portfolio construction processes. Leveraging the original Markovitz work, these fund managers quickly embraced the most innovative numerical solvers and computer power to move beyond an all-index constituent-matching approach. By selecting a reduced number of positions versus their benchmark holdings, managers can run small-dimensional (or “sparse”) portfolios that quasi-match the risk and return characteristics of their reference indices.

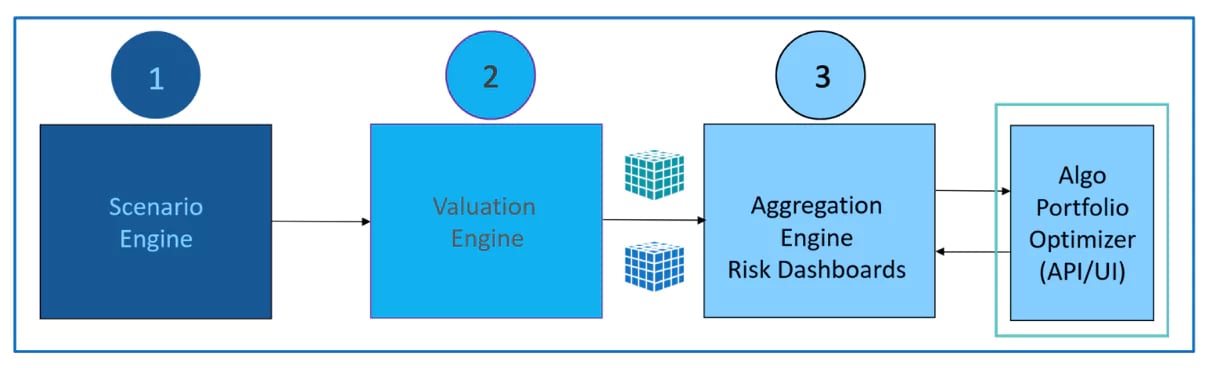

In the context of our latest SS&C Algorithmics research report, we review some of the trade-offs inherent to such a sparse portfolio construction approach. With a focus on corporate bonds, we first use scenario-based optimization techniques to generate a set of efficient frontiers. We illustrate the evolution of expected tracking errors versus the number of optimal portfolios’ positions. We then explore how selected supervised and unsupervised machine learning (ML) techniques can be used to improve our initial optimization-based sparse portfolio construction process. We compare our original and ML-enhanced optimal portfolio results with regard to ex-ante tracking errors versus position numbers. We recently extended the comparison metrics to include other portfolio indicators such as diversification ratios, stability of the asset selection and overall computational speed.

In conclusion to this study, we suggest future research directions, which include the investigation of market liquidity considerations and their impact on ML-enhanced optimal portfolio holdings.

To learn more about the ETF-related sparse portfolio construction approaches we have explored, download our "ETFs - Machine Learning-Enhanced Sparse Portfolio Construction" whitepaper.

Contact us to learn how you can use SS&C Algorithmics’ risk analytics and scenario-based optimization solutions in your own portfolio construction processes.